Skyrocketing tuition prices have forced scores of aspiring college students to take out loans in order to finance their educations. With graduates making 98% more per hour on average than people without a degree, attending college is an imperative to joining the middle class

In theory, loans provide a leg up for underprivileged students attempting to move up the socioeconomic ladder. However, the path to receiving a coveted diploma is often fraught with dubious lending practices and deliberate misinformation — to say nothing of the exorbitant price tag.

Even though more than half of Americans agree that the cost of college is too high, there are many special interests working hard to keep it that way.

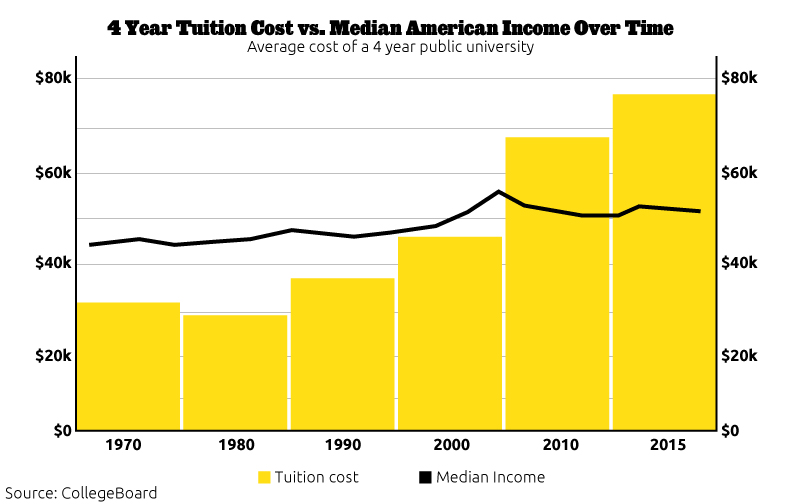

The cost of college has never been higher

In the past three years, the number of colleges and universities charging over $50,000 per year for tuition has increased by 2400%. During the same time period, the average wage of the American worker grew by a paltry 2%.

Working full time, an American making federal minimum wage makes about $15,000 a year, putting higher education well out of range — even in-state public universities cost an average of $23,000 per year. That’s four times the average price just ten years ago.

Unless you come from a wealthy background, there’s really only one choice: take out a student loan.

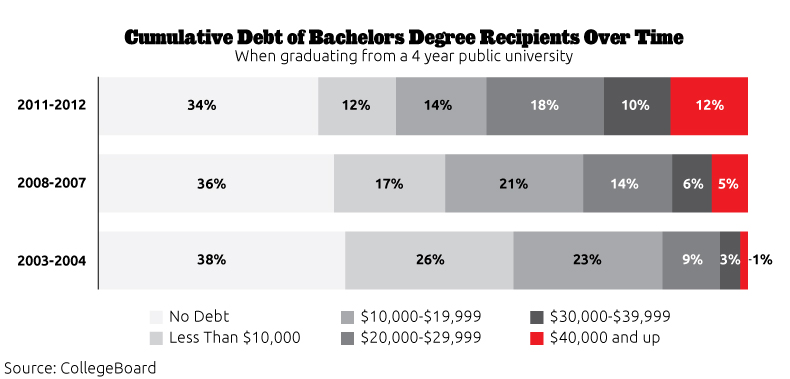

Student debt is at an all time high

Nearly 38 million Americans have student loan debt, totaling about $1.2 trillion dollars nationally. Student loans are now one of the largest sources of personal debt in the United States, outpacing even auto loans and credit cards.

The huge new source of debt comes with an outsized cost. Student loan debt is arguably one of the worst kinds debt out there.

Student debt hurts everybody

In the span of a single generation, student loans have changed from a useful mechanism for getting ahead to something akin to a modern form of indentured servitude. This, in tandem with the ever-increasing cost of attending school, has led America to a point where half of students who have direct loans are delinquent or late on their repayment.

There are shockingly few consumer protections in place to guard former students from facing the collector. Wages, social security, and even disability checks may be garnished by the Department of Education if a borrower falls behind on payments.

Alarmingly, even death is not an obstacle. Unlike other kinds of debt, which can be forgiven through declaring bankruptcy, student loan debt is a specter that may haunt graduates for life. If a debtor dies, many private lenders will strong-arm their mourning family into paying off the remaining amount in full.

The pressure on young people to shoulder the burden of such large debt so early in life has had a measurable impact on the rest of society. Due to uncertain financial stability, college-educated millennials are postponing major milestones such as purchasing cars, starting families, or buying houses – all of which are crucial elements of repairing an economy on the mend. From 2008 to 2011, only half as many young Americans opened new mortgages as compared to a decade earlier, creating a serious drag on economic growth.

Even as student loan debt contributes to the continued economic squeeze, there are plenty of those out there who stand to profit.

Why no reform? Just follow the money.

Low and middle-income students, with little representation in Washington, have been overlooked by the federal government for years. For all the lip service that politicians pay to the issue of student debt, very little action has actually been taken to remedy it.

This, of course, is what private lending companies such as Nelnet, Navient, and others, hope for. Their millions of dollars spent collectively on lobbying have long paid off in their continued relationships with the federal government. Sallie Mae has spent nearly $3 million on lobbying politicians every year since 2007.

The government, too, makes a profit off the backs of poor students. Through the use of intermediary collection companies, the government stands to benefit even on the loans that default. From 2007 to 2012, the Department of Education made $66 billion in profit, and are poised to make an estimated $184 billion total by 2019. A 2005 article in the Wall Street Journal uncovered that the federal government collected on average 100 percent of the principle of defaulted loans, along with an additional 20 percent in other fees.

The current student loan crisis is a prime example of the kind of shady ethics that result when government and private industry get in bed with each other. Without major, systemic anti-corruption reforms, you can unfortunately expect America’s student debt crises to continue.